What the Past Says About the Future

VRP, IV, and HV Autocorrelation

Setting the Table:

We still have an entire Friday session, but so far the week has seen some significant intraday volatility post FOMC meeting, with indices ultimately landing lower. (Hold on though!)

It’s not surprising to see ATM vol pop a little bit more as the rate hikes we were all promised look closer to fiction than fact. What is notable is this persistent trend of increased intraday (Parkinsons) vol in green. Since the start of April things stopped happening overnight and intraday vol even surpassed implieds.

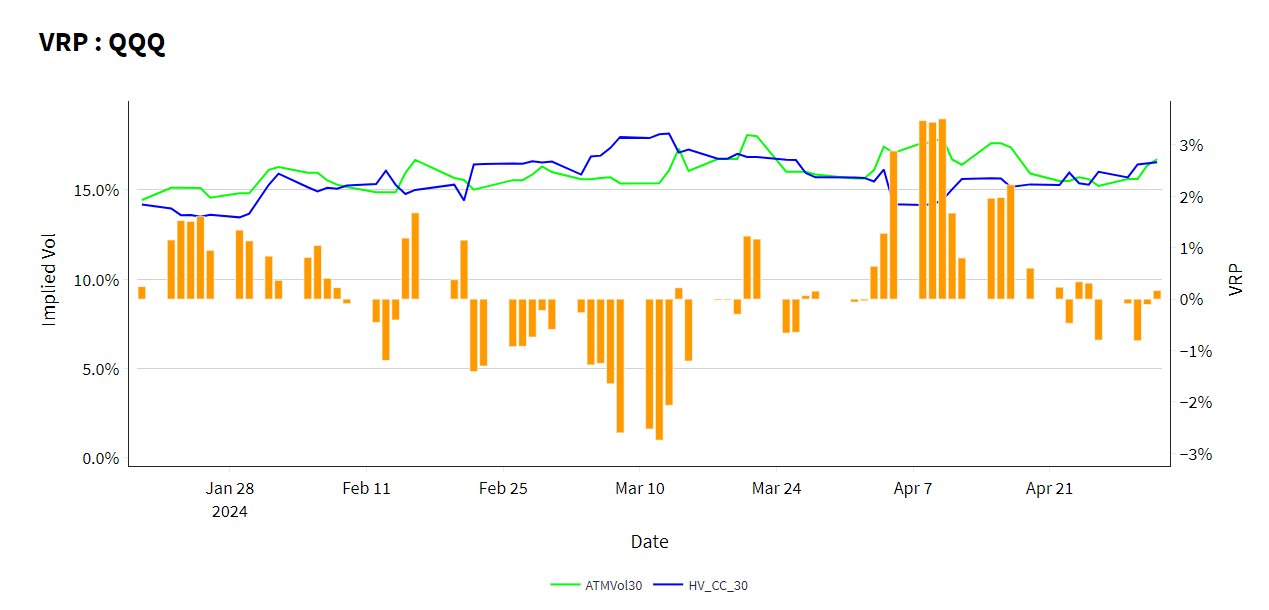

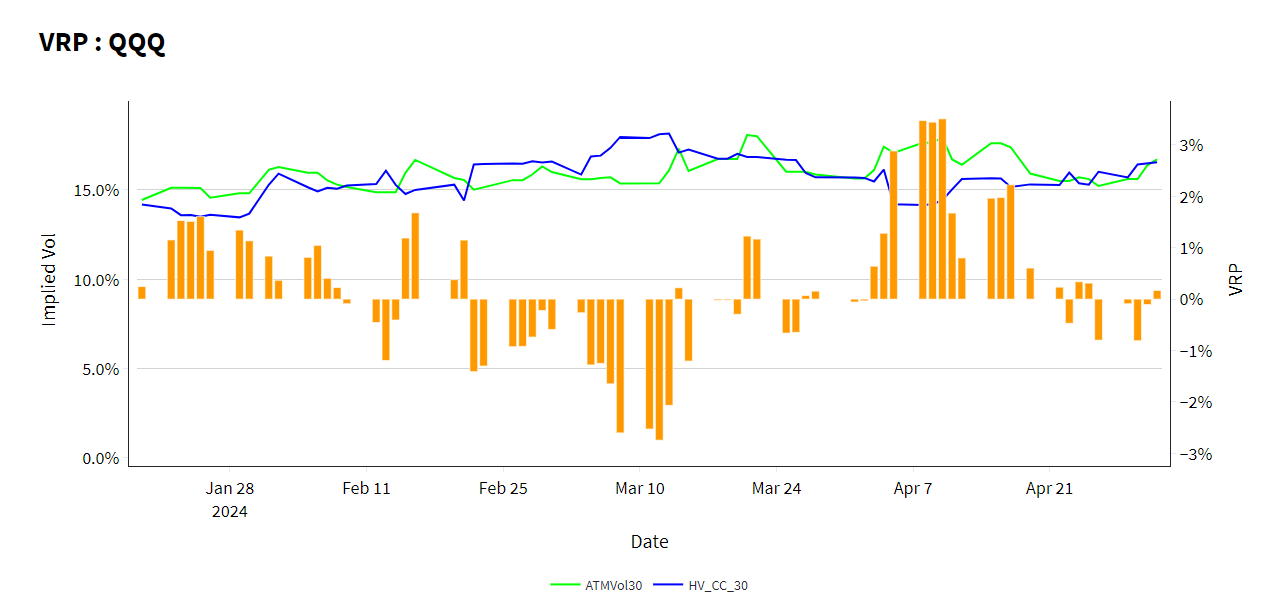

From a market efficiency perspective, QQQ has been pricing this all quite well. The net of implied and realized (VRP) is near flat for the last 2 weeks. While we had mispricings in both directions in early March and early April, that has flattened significantly. The QQQ options didn’t know what AAPL and AMZN earnings would be, or the Fed was going to give them, but the implied vol pricing pretty well nailed the realized.

Founder of options market behemoth SIG has some short and sweet opinions on the Fed. He believes that the intervention is not only increasing volatility in the markets, but raising the cost of capital. Through bond purchases they’re driving correlation - thus index volatility - higher.

Identify

We talk a lot about VRP because it is the statistic that best describes the efficiency and expectations of the options markets. While the path an underlying takes matters, that path is heavily framed by the most important pricing indicator in options - the implied volatility.

Very tight VRP in an index name gives me confidence to execute any number of strategies. Hedged equity like the GULL that only resets once a quarter can be confident that markets will be fairly reasonable. (Take a look at TheTape.Report though, here is SPY - GULL90 and they do vary!)

While VRP tends to be more variable the further out the liquidity scale - as we explored in VRP + Liquidity, Where Go Thee? - in the most liquid single names you can still remain focused on whether the trade or strategy fits into your and less about the exact pricing of IV.

I do use some qualifying words here, because even in the most efficient markets volatility is only “well priced” “most of the time”. Most and well are also open for interpretation.

One of the features of volatility that we’ve discussed before (Volatility’s Past Trauma), is how variance tends to be “conditionally heteroskedastic”. The theory behind the “GARCH” models for volatility, is that the best predictor of future volatility takes into account both the overall volatility this issue has seen, along with the most recent volatility environment.

If volatility is conditional on its current environment and auto-correlated, can we say the same for VRP? Does that make it valuable as a predictor?

Keep reading with a 7-day free trial

Subscribe to Portfolio Design with TheTape to keep reading this post and get 7 days of free access to the full post archives.