Hedged Equity: WBA, GILD, ABR

Dividend Screener Results: July 2, 2025

Setting the Table:

Futures are lighter this morning as we delve deeper into the holiday week. It’s a slow market (though 42M contracts did trade yesterday), which means it’s a good time to review longer term allocations or hunt for mispricing.

As we look at longer term pricing, an interesting trend has continued with QQQ volatility over the past month. The price of the COND90 has continued to tick up - increasing almost 15% since June 1st. (1.35% of stock price to 1.53%)

This week in Portfolio Design, we’re using the lens of our Dividend Screener and today the focus is on medium term Hedged Equity (GULL90). The objective here is to identify names which produce cash flows but also have attractive options structures.

We use the following columns in our screen: LIQ, GULL90, HV_CC_90, ATMVol90, VRP_CC_90, IVnetHV90, DivYield%, and Bolly100STD1. Find all the definitions here. We also limit this to only LIQ250 names.

We’ve shifted the VRP/Vol indicators out to 90 days, which corresponds with our longer dated GULL target.

While we’ve sorted by the highest GULL90 readings, I’ve included a minimum dividend yield of 4%, so we’re seeing high yielding names, with expensive options structures.

At Portfolio Design, we track opportunities through four different lenses: Volatility (VRP, IVNetHV), Liquidity (LIQ), Momentum/Mean Reversion (Bollinger) and Dividends. Each of these filters represents a different approach to investing, and can be used independently or in concert.

With these frameworks in place, follow along here twice a week as we dissect what the screens are telling us for Covered Call and Hedged Equity structures. Identify both short term trading and longer term investment opportunities. Free subscribers get a taste with “YIKES” and paid subscribers get analysis on the details of these opportunities, along with the full screener results.

Data comes from TheTape.Report where users can build their own screens and access a full suite of options indicators.

Yikes Again: RILY

No surprise, RILY also sits atop the GULL90 readings for dividend paying LIQ250 stocks. This is basically the same thing going on as yesterday.

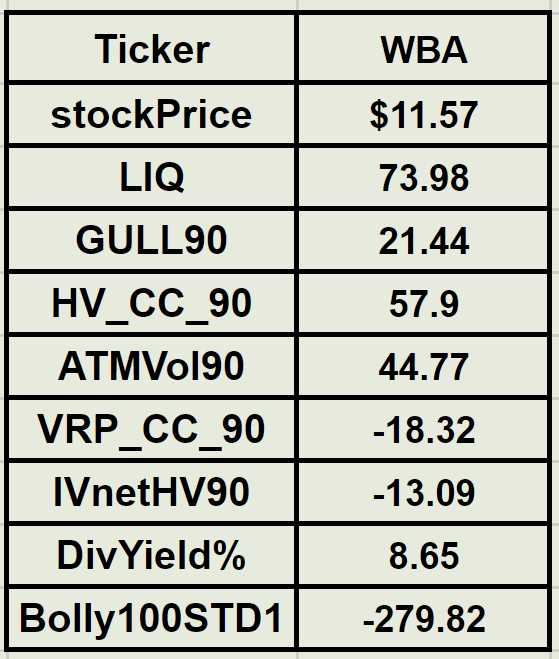

Yikes: WBA

WBA is a yikes stock because it is so deceiving. There are solid liquidity readings, and a very healthy dividend yield. But since the start of 2022 it’s down over 80%. Even in the last 100 days, it’s 2.7 standard deviations below the mean.

These readings are difficult because there’s not a good expiration fit out 90 days. While in the front month there are better listings at $0.50 intervals, $2.50 out 90 days makes this structure impossible.

If you’re looking for a rebound play on this, unfortunately there’s not a good way to protect the downside with these strike listings, and either select a different stock or choose a shorter tenor.

Keep reading with a 7-day free trial

Subscribe to Portfolio Design with TheTape to keep reading this post and get 7 days of free access to the full post archives.