Calibrating for Skewness

How to think about covered call allocations in your portfolio

Setting the Table:

Vol is up 33% in the last ten days! Now a thirty day ATM reading of 15% or a VIX of 17 is hardly markets in turmoil, but it has woken up investors lulled by a sleepy summer. Saying it’s up some huge percentage isn’t as relevant as understanding that annualized implied variance has risen by 3-4 points. More, but not a LOT more.

Compared to the slow grind up we’ve had, Tuesday dropped and kept going. Yesterday was a strong rebound that failed and turned back lower. As things start churning, the path the market and pricing inputs take on a day to day basis gets significantly longer.

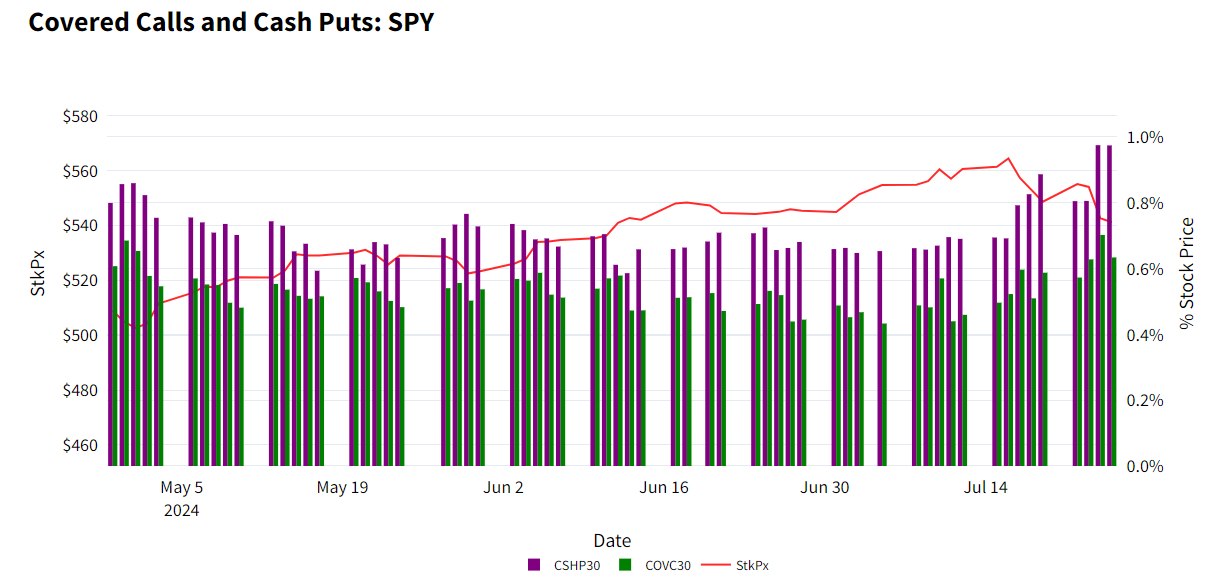

When vol perks up, so do covered calls and cash puts. COVC30 is up about 30 bps in the last ten days for both QQQ and SPY.

That means a good deal more cash to collect today. On SPY, 30 bps of additional premium is $162 in your pocket for every contract on the 30 day option.

It also means there is more distance for the same delta - the 30 delta call closed yesterday $14 out of the money (2.6%), whereas on July 15th it was $11 (1.95%).

Here’s another plug about strike listings - on July 15th SPY only had the $572 and $575 strikes listed. While now those dollars have been filled in - even thirty days out you were forced to choose between the 28 delta and 33 delta.

But what happens to the position if you traded a week ago? That would have been very reasonable to trade on a serial expiration! (See - Splitting Apart Strike Scores).

Imagining you had the foresight to shade your delta higher, and sell the $572 strike at $3.70 - it’s now only worth $0.38. Assuming this was Bought/Written, the PnL on the trade is down $22.76 on the stock, and up $3.32 on the option - a net loss of $19.44 per share.

Further, the position has materially changed - the delta of that short call has plummeted to 5. Don’t forget the short gamma - covered calls get longer deltas as stock goes down.

What do we do next? In this week’s Portfolio Design, we’ll analyze how to manage and think about portfolio allocations with covered calls.

Sitting at a market maker desk, the arithmetic is simple. Long 100 shares of stock, sell a 30 delta call, the position is now long 70 deltas. To get delta neutral, sell more calls, stock, or buy a put. Do more of this as stock goes lower. The goal is to be flat. For options investors, the calculus might not always be so simple…

Keep reading with a 7-day free trial

Subscribe to Portfolio Design with TheTape to keep reading this post and get 7 days of free access to the full post archives.