The Election Hedge

Fifty Ways to Trade an Option

If you didn’t know, the United States is having an election in just about two weeks. As far as anyone knows it's a toss-up.

The polling has remained tight, but prediction markets have shifted decidedly pro-Trump recently after Harris sat dominant for several weeks after her selection. There is some evidence of whales manipulating the prices here, though I tend to trust capital at risk over opinions on the phone. Who knows.

What the options markets do agree on is the fact that this is going to bring some volatility. Whether that’s due to disputed results or capital shifting based on expected policy, election volatility has been foretold for months.

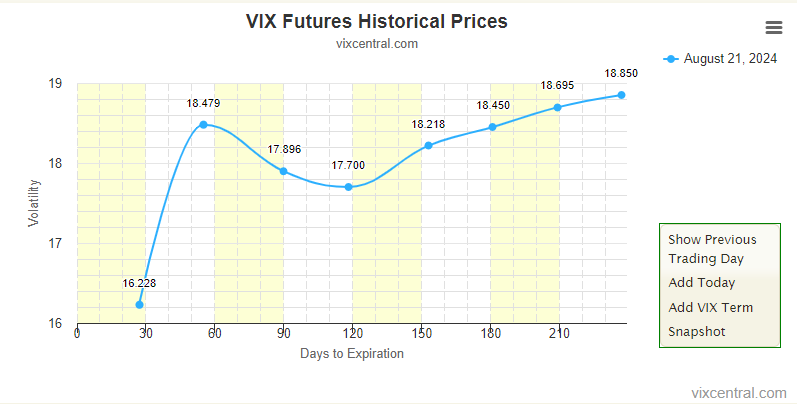

The VIX futures curve prices what the VIX is expected to be on a given day. Since the VIX is forward looking 30 days already, we expect the VIX a month BEFORE the election to have additional premium, and that’s been the case with the October contract all along.

Above we have the term structure from two months ago. While back months tend to trade over front months in “normal” scenarios, this contango has a curious bump, where the October contract is notably above the December or January.

Another effect of this is that volatility is going to decay somewhat differently. Like any earnings or FDA announcement that is well telegraphed, we all know when Election Day is. The VIX or implied volatility seen in your options montage are single figures that describe the distribution across the entire period. November 2 and 3 are likely to be much calmer days than November 5th or 6th.

Options positions that are expiring after the election will see some curiosities with their decay. As that election becomes a more significant component of the time remaining (i.e. election day vol is 1 of 4 days rather than 1 of 50 days) the options will see less “theta” come out, as the straddle remains relatively constant. No matter what the greeks say, that call and put combination will reflect the market expectations of moves for that time frame.

This makes putting on a position around the election more nuanced. Event protection is always more expensive, so we need to think about ways to offset the price by giving away risks we’re comfortable with, whether that’s upside, downside, or something in between.

Today in Fifty Ways to Trade an Option, we’ll explore ratio hedges that reduce cost and offer event specific pay off scenarios.

Keep reading with a 7-day free trial

Subscribe to Portfolio Design with TheTape to keep reading this post and get 7 days of free access to the full post archives.