Setting the Table:

Futures have rebounded solidly this morning after dipping nearly 80 points just before the East Coast went to bed. Escalating tensions in the Middle East has the market looking shaky and volatility catching a bid.

SPX is set to open flat , and VIX is only up a measly seven cents. But the overnight session got perky!

Now it makes sense why the CBOE pays market makers in the Global Trading Hours a cash incentive with discounted transaction fees!

The VIX is reading higher than it has been all year, but additionally the volatility of volatility has increased. The VVIX index measures the VIX of VIX options, and this April things have been cooking. N.B. This will mean revert faster than the VIX.

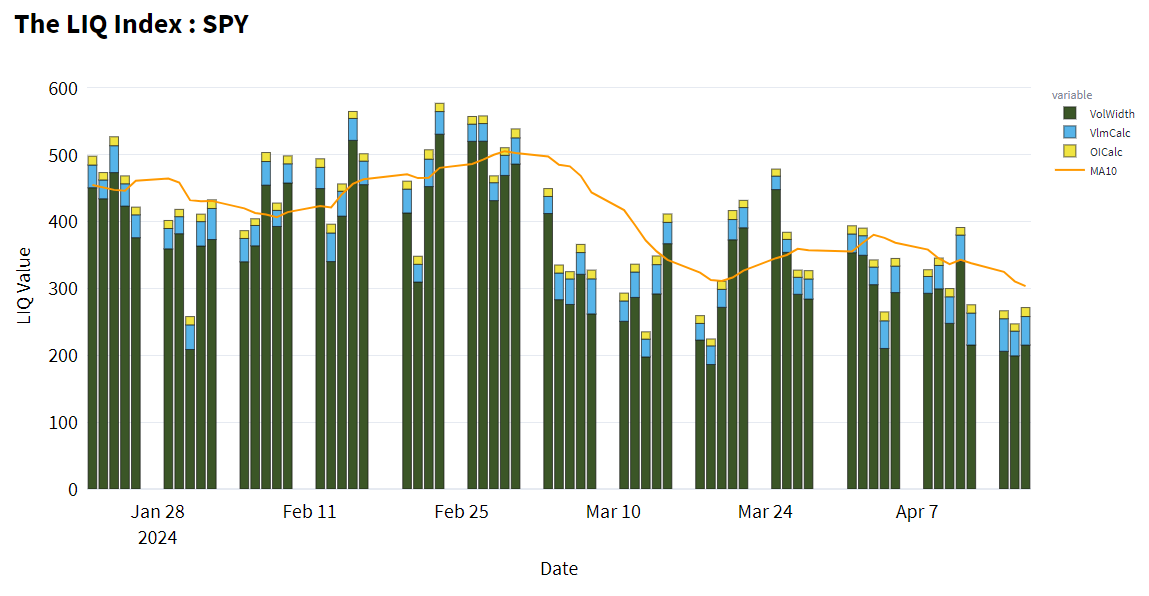

Liquidity continues to fall off faster than vol is spiking. Global conflict increases volatility, but more importantly introduces uncertainty about the price of volatility. As implied volatility or the VIX move up, in order to justify and sustain those levels, there needs to be ongoing and significant realized volatility. (A VIX of 20 means roughly 125 basis point moves every day). When vol first starts to lift off, spreads are going to get wider as participants bake in a little bit more fuzz into their pricing.

Identify:

If you haven’t been thinking about hedges this week, congratulations. Most of the world however is long only, and has likely seen everything from their 401(k) to their play account take a hit.

You can hedge your stock with options, or your options with stock. Even options hedge options, and some stocks hedge others. The purpose of a hedge is simple, to reduce the variance in your PnL so you can compound faster. Hedges balance out the known risks, so that you can isolate a specific exposure.

An old joke on the floor was “why waste the edge with a hedge?” While cheeky, and likely to irritate the risk manager, there is a kernel of truth. If you spend your time covering every possible risk, you’ll end up paying for exposure.

The tools you use, and the amount of exposure you cover with a hedge will depend on your strategy. Sometimes the best hedge is none at all.

Let’s dig in to how to hedge underlying equity positions (GULL, COVC), leveraged positions (FALC) , as well as market neutral condors (COND).

Keep reading with a 7-day free trial

Subscribe to Portfolio Design with TheTape to keep reading this post and get 7 days of free access to the full post archives.