Setting the Table:

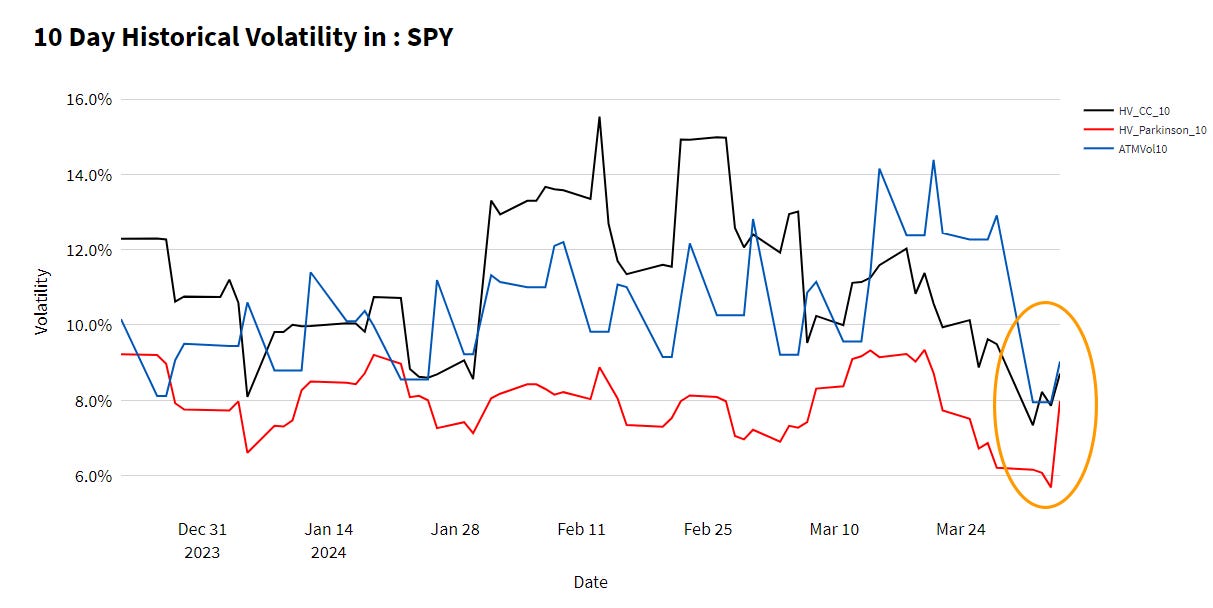

Markets saw their first real day of volatility in over a month yesterday with the SPX turning an 80bps rally into a 123 point drop. That’ll get the Parkinson’s intraday volatility going.

Everything “spiked” yesterday on the turn around, but we see the most movement in the intraday vol measure.

The last 10 days for the SPX look like a “mesa” where we rallied hard, stayed flat, and then dropped it all back. A few days with big action, but mostly a tight range of $5.

While we popped yesterday, the reading of 8% on a 10 day horizon was still lower than it was in early March, because there consistently was a much wider range.

From a strategy perspective, the very recent environment made 0DTE or shorter dated options quite interesting. Implied volatility has not come down, but other than yesterday, we’re mostly seeing tight ranges. Short term premium capture is much more difficult when intraday volatility is relatively high.

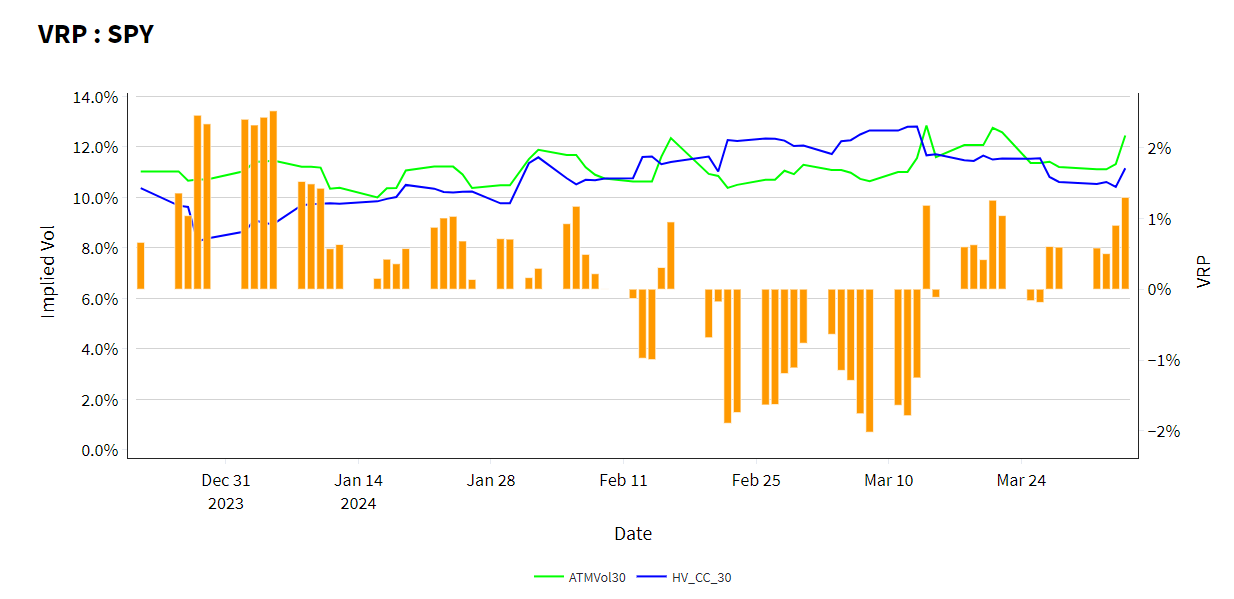

We spent much of this year observing a negative VRP environment for SPX, but as we’ve started to see some movement the past few days, that value has actually increased. The market saw implied vol slowly rise throughout the negative VRP environment in March, and now better priced these movements.

All throughout this time period, the SPX has risen steadily. Q1 returned almost 11%. We typically see a very high negative correlation between SPX and VIX (spot up, vol down) on the order of -80% to -90%. However vol has gone the opposite way.

Jim Carroll points this out using the SVIX (a short VIX futures ETN):

Identify:

While yesterday’s movement doesn’t quite yet constitute a regime shift, it does highlight how quickly vol pricing might change. The 30 day condor in SPY jumped from 62bps to 74bps of the stock price in one trading session. That’s a 20% price increase - not just because stocks were on sale.

There are spikes all the way along, which highlights the importance and randomness that timing can have.

With the first quarter in the books, this week is often a rebalancing time for strategies. The most popular hedged equity trade reset last Thursday, and timing again is an issue for a trade like this. The GULL90 tracks the put spread collar here, and while it looked like there was going to be a lot of headroom at the end of March, that value has fallen almost 100 basis points.

Looking at stable skew, the difference is visually subtle, but produces a meaningful pricing difference. The below is the 90 day IV curve. The difference at 20 delta is only a 50 bps increase, while at 80 delta it’s a 130 bps increase. Those are roughly the levels that the GULL90 would be targeting, and you can see the more vega intensive put in the spread has gone up more than twice the call implied volatility. That means the strategy has to sell a closer to the money call, because they’re mandated to rebalance at the end of the quarter.

Whether you’re selling volatility, or protecting your portfolio, timing matters for these strategies. You can’t avoid exposure, but you can do your best to mitigate the impact that a strategy rebalancing has on your performance.

Let’s dig in…

Keep reading with a 7-day free trial

Subscribe to Portfolio Design with TheTape to keep reading this post and get 7 days of free access to the full post archives.