Skew for Sale

Risk Reversal Premiums as Vol Drops

Setting the Table:

A lot can happen in a week, as the news from the Federal Reserve and Bank of Japan has proven. While we were staring at an abyss below 4000 SPX heading into Halloween, the market spooked to the upside and has gained over 200 points since last Friday’s close.

Volatility has been absolutely crushed as a result. Part of this is because the event has passed. Even if the market didn’t move at all, we’d expect for volatility to come in, but all that and more has happened with the strong rally.

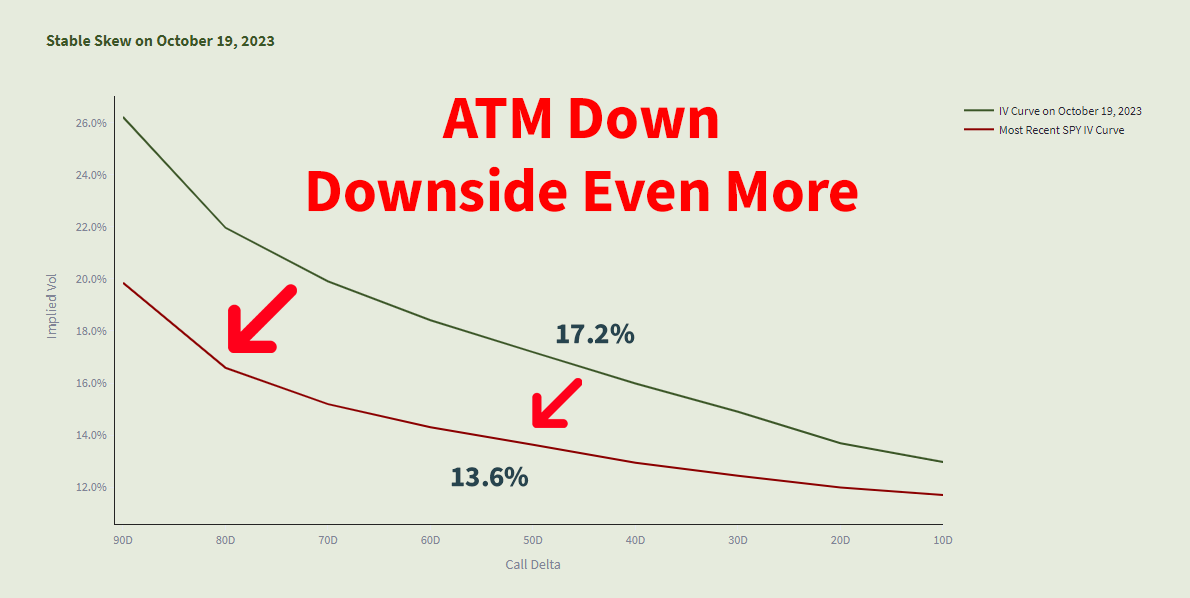

The last time that SPX was at 4300 was October 19th. ATM Vol on 10/19 was about 17.2% while yesterday it closed at 13.6%. (The new StableSkew History Mode allows you to see what a curve was on a given day (Dark Green) and compare it to the present (Red). ) ATM vol is down, the downside is down even more.

For those interested in doing a deeper dive into some options readings, here are a few links that I’ve found interesting this week. Please reach out if you’d like to discuss!

A Devil's Bargain: When Generating Income Undermines Investment Returns

Roni Israelov and David Nze Ndong analyze whether higher premium options generate higher returns for covered call strategies.

Structured Retail Products: Risk-Sharing or Risk-Creation?

Do structured products for retail investors generate net value in the form of risk sharing, or are they introducing systemic risk to the market?

Identify:

As implied volatility has come out of the market, historical volatility has also settled down. While on a given day these movements feel significant, as the horizon moves from 10 to 30 days (or further) these become more muted and a 17% implied volatility is actually too high.

Another interesting indicator for the S&P 500 is that for the first time in a while we see that back month volatility is over front month. This state of “contango” is the most common. Usually the near present is well known in vol space, while further out we can expect something to happen. It’s only when a big event or panic happens that the market moves into “backwardation”.

The RAVN indicator here is saying that the average value for the difference between the monthly (30 day) and weekly (7 day) option (RAVN30) has been right around flat (0.02%). After the FOMC meeting and resulting vol crush, that spread has widened to 7/10ths of a vol point. That doesn’t sound like a lot, but this spread does increase further out, we’re parsing the very short end of the term structure here.

Keep reading with a 7-day free trial

Subscribe to Portfolio Design with TheTape to keep reading this post and get 7 days of free access to the full post archives.