Setting the Table:

Fans of early 90s punk rock will be celebrating - not only because they own a lot more stocks than zoomers - but because we’ve seen nothing but Green Days for the past week. Despite bad earnings from TSLA, there’s no call wall too strong in the broad market. Markets opened flat today - let’s see whether it continues.

While close to close values have all been positive, two of the four days so far this week have closed lower than we opened. That means the price increases are happening in the overnight sessions. Parkinsons historical vol calculation in red has been persistently below the black like which is the traditional close/close metric. Intraday ranges are less than what’s happening out of market hours.

Jason, Lex, and I talked a bit about this at the end of our show yesterday. Would you rather sell a 1 DTE or 0DTE condor/butterfly?

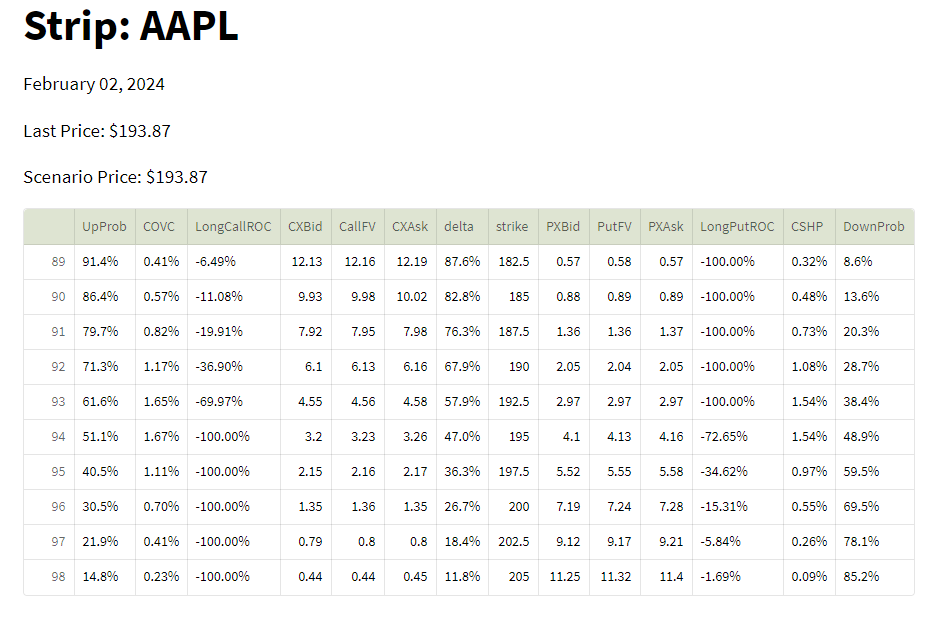

Subscribers can take a sneak peek this weekend at a brand new feature called the “Strip”. This grabs live market data, calculates the probability of a stock crossing a strike based on historical data and shows the returns of a Covered Call/Cash Put strategy in various price scenarios. It gives indicative markets of where you’re likely to get executed. Build a single leg or complex trade, with expiration PnL charts and tracking ability for when to close or roll the position.

Yesterday in TheTill, I wrote about “who” sets price: Price Set is Price Paid. Dealers are actually very hesitant to set a price, they want to trade around a price.

Identify:

Much of the chatter about flows this year has been about the amount of volatility supplied to the market, particularly on the upside. The theory goes that in order to protect valuations investors have put on equity overlays that have the effect of suppressing upside and ATM volatility.

These can be done as a simple covered call - arguably the most effective options strategy discussed last week - a zero cost collar, or some form of put spread collar like the GULL trade.

One of the hypotheses is that this investor selling leaves market makers in a long position, which means their hedging activity is likely to suppress upward price movements. While that might be true on an intraday basis, I wouldn’t count on dealer positioning to defend overwhelming flows - in either direction.

The reasons for a protective overlay can be both situational (relative to spot level), but also procedural at the end of a calendar year or quarter. Regardless of the motivation, the overall level of forward rates - with a dash of skew - will tweak the outcomes here.

Keep reading with a 7-day free trial

Subscribe to Portfolio Design with TheTape to keep reading this post and get 7 days of free access to the full post archives.