Diversifying Your VRP

How variance correlates across asset classes

collections. The image should vividly represent various investment elements: gold bars, an oil barrel, a stylized representation of Bitcoin, and bond certificates. These elements should be surrounded by assorted financial and mathematical symbols, along with trading icons. The background should subtly include graphs and numeric data, emphasizing the theme of strategic investment in a complex market.")

Setting the Table:

Markets have been moving. Realized volatility is back over implieds, but most significantly, this is happening during the day. Overnight returns contribute to quite a bit of the movement in the market.

We can measure VRP as implied volatility versus multiple different versions of realized volatility. The “Close to Close” method encapsulates both overnight and intraday - it snapshots the market every day. Using the Parkinsons method with intraday highs and lows, we typically see a lot more consistently positive VRP - part of the price of volatility is the overnight move.

Compare this to Close to Close below where we’re used to seeing a lot more chop. But the recent intraday ranges have been pushing even Parkinson’s VRP measure down.

Identify:

We tend to talk mostly about equity volatility here (index or otherwise), but with ETF options we get several good proxies for other asset classes. As with a portfolio of the underlying assets, it can be useful to consider options structures for the same.

Any long holder of an asset can benefit from an overlay. Whether it’s a covered call, put spread collar (GULL) or some combination of both (HRON), using options to neturalize part of your exposure and make risk/reward trade offs is interesting.

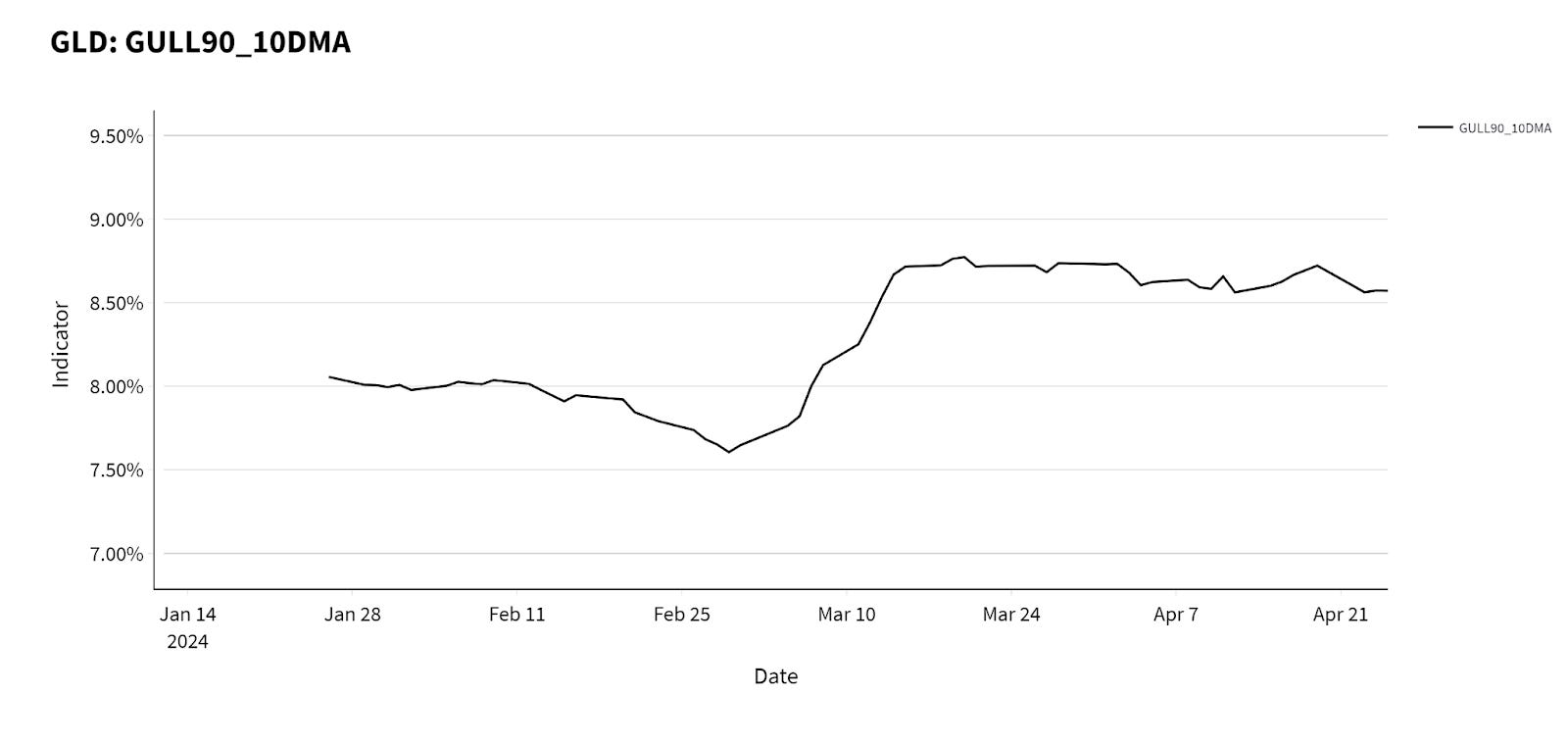

Gold has perked up recently, as has the value of the GULL. GLD does a pretty good job of tracking the price of physical, and we can see that the standard 5/20% put spread collar is funded an 8-9% OTM call. That’s roughly in line with a name like BAC.

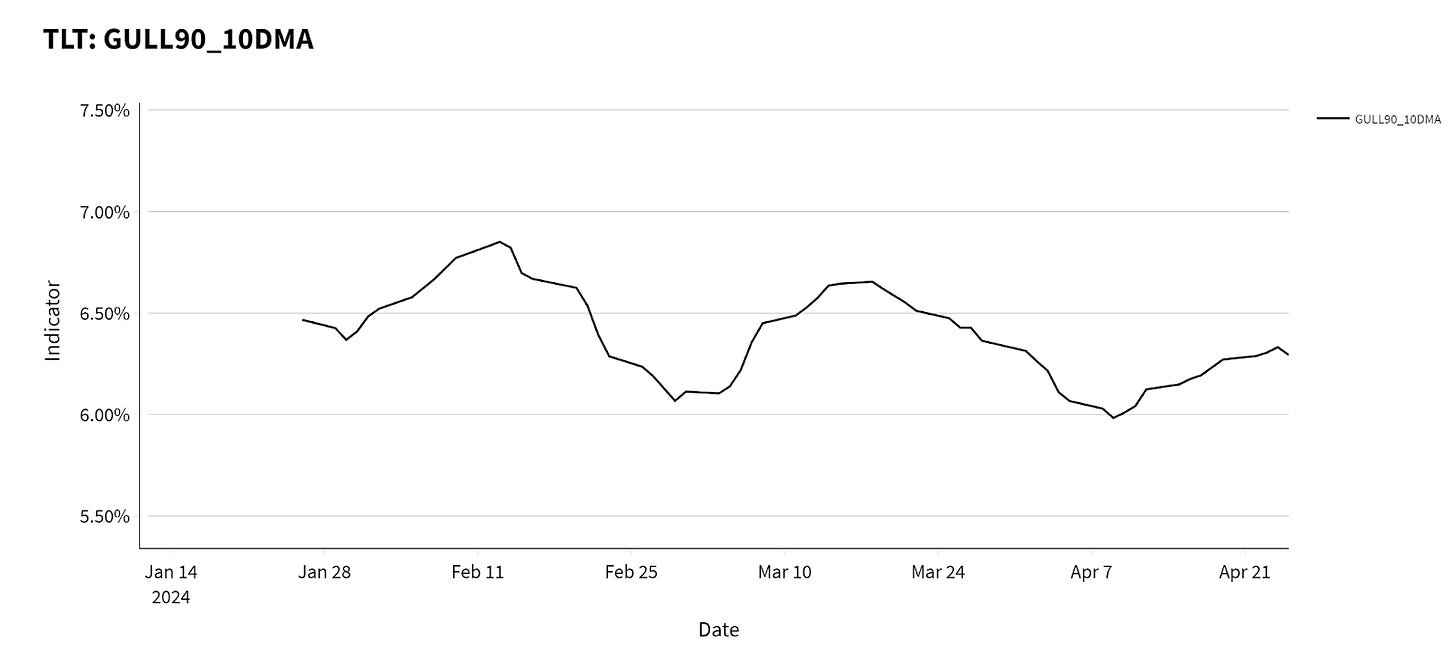

The GULL in TLT is only slightly above what the pricing is in SPY.

If you want upside, you’ll get it in BITO. The pricing of the futures roll in the ETF makes it less significant than in direct options, but there’s a decent call skew from upside buyers. Plenty of speculative energy behind the pricing there.

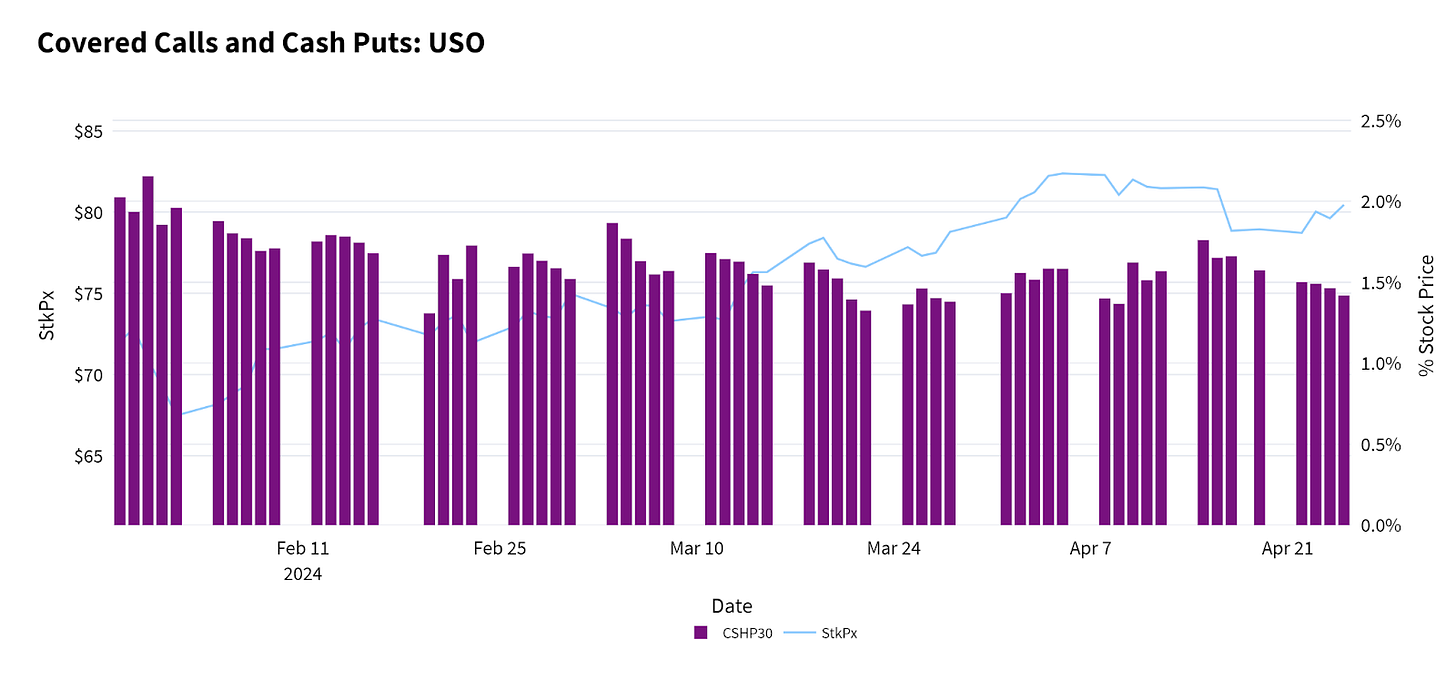

Rather than hedge the price at the gas tank with long USO, you can consider writing puts here as a VRP/delta play. They trade for almost 2x as much as they would in SPY.

When we’re talking options, we’re talking volatility. If we want a 60/40 portfolio of stocks and bonds because they balance out, does the same hold true for their volatility and variance?

Keep reading with a 7-day free trial

Subscribe to Portfolio Design with TheTape to keep reading this post and get 7 days of free access to the full post archives.