Covered Calls: CGC, SIRI, BYND

Using volatility metrics (IVnetHV and VRP) for trade opportunities

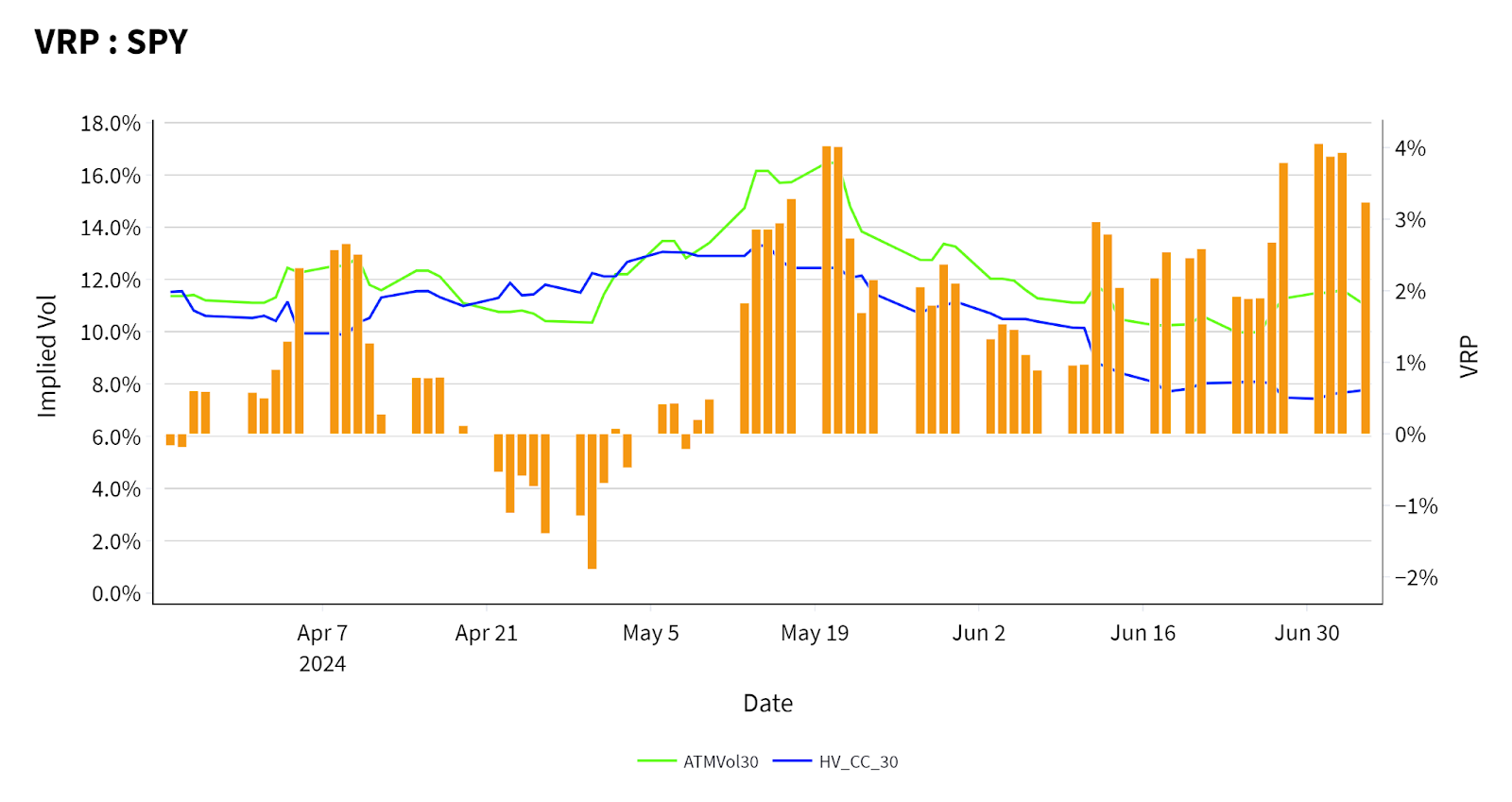

Setting the Table:

Volatility markets tend to be boring around the holidays. It’s nice when equities hit all time highs, but the options markets have been fairly tepid in response. My 30 day ATMVol alerts for SPY are back to single digits (9.8%) as implieds follow realized downwards.

Looking out 30 days, this has led to continued and significant VRP in SPY. That’s not always the case on the shorter time frames, as on a day like Friday, the 30 point SPX rally nearly doubled the incoming one day straddle.

In summer markets with thin premiums, the difference between IV and HV can point us towards interesting opportunities.

For an in-depth dive into how 1 DTE straddles perform during this time period, check out Vol Vibes by Michael Hunt.

This week our overlay analysis will focus on differentials between both past volatility predictions (VRP) as well as differences in the market’s forward looking opinion (IVnetHV). This can be useful for identifying both trading as well as investment opportunities, where persistent small trends indicate stable excess premiums, while more extreme gaps suggest a more immediate and dramatic reversion.

For our Screener choices, we’re going to use the following:

With all trades it’s important to have a concept of the underlying business environment. However this is particularly with implied volatility pricing opportunities, and thus we explicitly include the Industry detail.

The opportunities today look more like “Trades” with earnings expected in roughly a month for both BYND and SIRI. Both suggest comparing the implied volatility levels across the term structure and is a good case for where our indicators signal opportunities, but the markets define our strike adjustments.

At Portfolio Design, we track opportunities through four different lenses: Volatility (VRP, IVNetHV), Liquidity (LIQ), Momentum/Mean Reversion (Bollinger) and Dividends. Each of these filters represents a different approach to investing, and can be used independently or in concert.

With these frameworks in place, follow along here twice a week as we dissect what the screens are telling us for Covered Call and Hedged Equity structures. Identify both short term trading and longer term investment opportunities. Free subscribers get a taste with “YIKES” and paid subscribers get analysis on the details of these opportunities, along with the full screener results.

Data comes from TheTape.Report where users can build their own screens and access a full suite of options indicators.

YIKES: CGC

The LIQ score is the main indicator that something might be difficult to trade, despite seeing some pretty attractive indicators. The rub here comes down to strike settings, and wide markets.

The VRP and IVNetHV seem very attractive in the 30/40 range. Vol has been overpriced in the past, and we’re expecting to see that continue in the future. This is further displayed by the 5.74% you’ll get from a 30 day overlay at 30 deltas.

Something also to watch out for with covered calls, is that the short term trend has been significantly down. The long delta could hurt you as much as the premium collected.

$0.50 strikes that are nearly 9% of the stock price apart, combined with $0.20-$0.30 wide markets mean even if that premium exists, it’s going to be really hard to find a strike setup that works.

Below with StrikeFinder we can see that the max returns on the opportunities nearest to our target (30 day, 30delta) range pretty significantly - as low as 8% or as high as 44% depending on your strike and tenor selection.

Keep reading with a 7-day free trial

Subscribe to Portfolio Design with TheTape to keep reading this post and get 7 days of free access to the full post archives.