The Trend Mute

There's a very good reason people suggest to keep it simple stupid. The naive expectation for risk assets repricing after the Fed cut rates was the correct one. Money gets cheaper, stonks go up. While there were several hours when the overthinkers watched in glee as the markets faded the news, the subsequent rally to all time highs was decisive.

Take all this with a grain of salt - we’re less than 72 hours into the digestion. But the early trend has firmly spoken, and I hope you weren’t short too much upside. Long term investors have it easy - nothing to do or see here. Even if you’re short a call with a GULL, that’s a bullish strategy - no FOMO allowed.

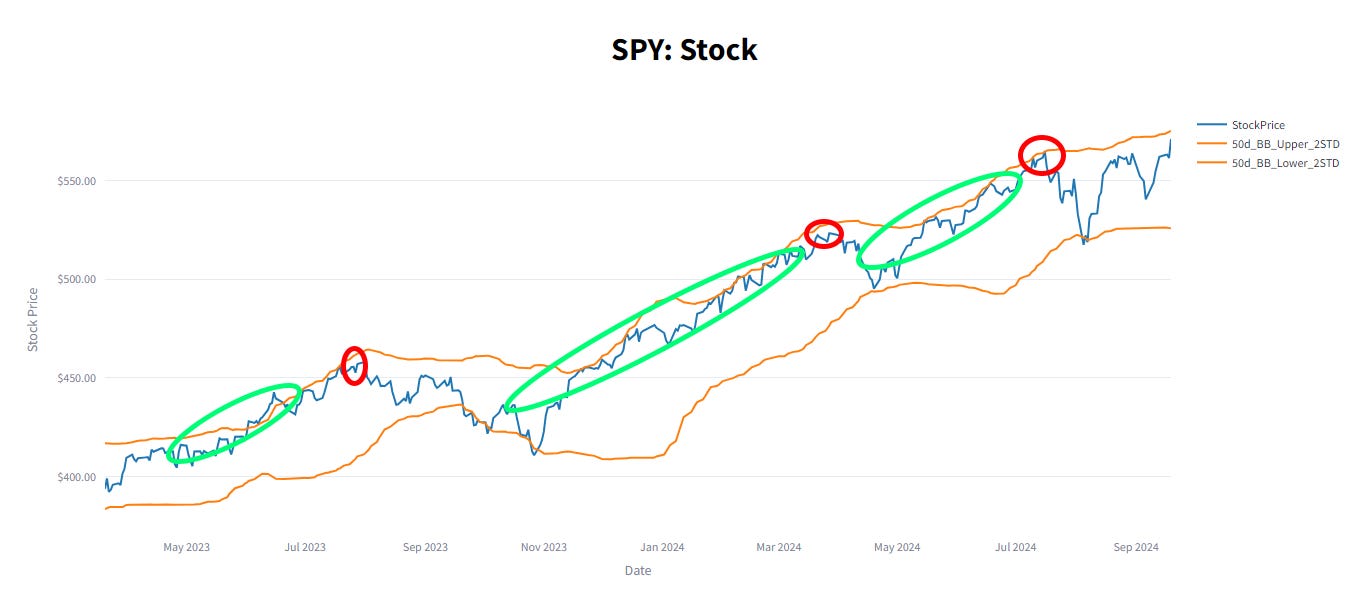

For those of us who like to watch a seismograph under a microscope, it feels like the path is up and off the charts. There’s a lot of rumbling about overextension and calls to fade the rally. Visually we see this as bumping against upper bollinger bands.

But for everyone who sees those red dots and wants to call for a retracement - remember how long we can sit in a nice green uptrend. If you want to be a contrarian, do it in small doses. No one picks the top with one great call, it’s a lot of trial and error. Sure put spreads just keep getting cheaper (whether you’re looking at vol or delta), but you also have to respect the collective market opinion.

In this week’s edition of Fifty Ways to Trade an Option, we’re going to look at a trend muting strategy. While it could theoretically be used on the whole portfolio, this strategy is for the itchy fingered nibbler. Market timing introduces more risk, but if you’re confident in your indicators and thesis, the Trend Mute can also juice returns.

Trend Mute:

Buy and hold investors - myself included - tend to get nervous as the market keeps going up. While we all like green numbers that are bigger than yesterday, downside risk has a gravitational pull. The further and faster we pull away, the bigger the scaries.

There’s an itch to do something - if I can just lighten up here, and then add more at the inevitable pull back, it’s free money. To be clear, it’s not. You’re adding a lot of risk. But sometimes there are screaming signals you can’t ignore.

When these opportunities present themselves - it's certainly not an evergreen strategy to fade a market that compounds at double digits - it’s extremely important to stay small and short term. Swinging for home runs is going to leave expensive strike outs.

The trade horizon isn’t just about being able to quickly correct if you’re wrong. But that is important. Options measured in hours to expiry have the most bang for your buck greeks. Long term volatility is expensive, and if you want the convexity payout on that inevitable drop - stick to the closest DTE possible.

Similar to strategies like the HRON, this structure is about taking more risk and execution management to capture some of the term structure. Trend Mute is at an even shorter duration, but the idea is the same to use a short term call (spreads) to finance longer term put (spreads).

While it doesn’t have to explicitly overwrite a position, there is a fundamental assumption that an investor is naturally long. Whether that’s in a retirement or brokerage account, the “mute” part of the name is because this will dampen the swings of your underlying position.

A good starting place for this structure is to sell a 5-10 delta call in the 0DTE options, to purchase a put spread approximately 30 days out. Levels here may vary based on paranoia, but the 25-30 delta level is a good start.

Turning this into a put spread reduces the cost of your protection (more so than the equivalent call due to skew), allowing you to push down the call delta and sell something further out of the money.

Over the course of 22 trading days, the premium generated from the short call will pay for your downside peace of mind. You’re sacrificing the further upside - but your thesis doesn’t think that’s as likely. Or you’re just comfortable giving that away.

Remember that cheap greeks cut both ways. On a 2% rally day, the 10 delta call in SPY will turn from $0.20 to $5. And even without a big rally, expect to get called away at least 2 or 3 times.

Turning the short call into a spread makes this look more like a “Sling Shot” trade, though it’s not as helpful in the 0DTE space. Selling a spread will return less than a naked option, therefore purchasing less protection. And to increase the credit side of the equation, you’re putting a spread very far away and are highly unlikely to realize anything above this.

This trade will be fairly sensitive to volatility environments. The 0DTEs have a lot more “IV” to them, but it’s also the most variable. Even at 10DTE we’ve seen what taking the Fed meeting out does.

While big macro events are somewhat the exception (does it feel like we are having more?) your options there are going to be nearly twice as expensive. That seems tempting, but it’s also a good day to simply sit out.

This structure is a series of trades, but it’s not a position to keep rolling. Thirty days is already a long time to be predicting short term market movements, so to consider rolling the put spread back out would require strong self critical conviction.

However there can be adjustments if the trade either works in your favor or against. If the market rallies and you’re still bearish, pulling up the spread for a debit lets you participate sooner in a drop.

Because of the nature of daily vs. monthly options, it’s possible, even likely, you’ll quickly offset significant portions of your put spread premium. One option is to just stop, and enjoy the free put. Alternatively, you can tweak the amount you collect, selling increasingly cheaper calls as this trade funds itself.

Applying the Trend Mute strategy should start out as a play account trade until you’re comfortable with what this does. As much as signals might scream red, playing into bear traps gets expensive too. But tactically lightening your long when the time is right - that’s exactly what options are great for.