Covered Calls: KSS, PFE, MPW

Covered Calls: KSS, PFE, MPW

Trading dividend stocks with earnings and low dollar handles

Setting the Table:

This week we not only have reports from four of the Mag7, but there are significant monetary policy announcements both domestic and international. Fed dot plot watchers are still pricing in a 90% chance of a September cut - it’s all about the commentary here. Japan and England are also on the radar for Wednesday and Thursday.

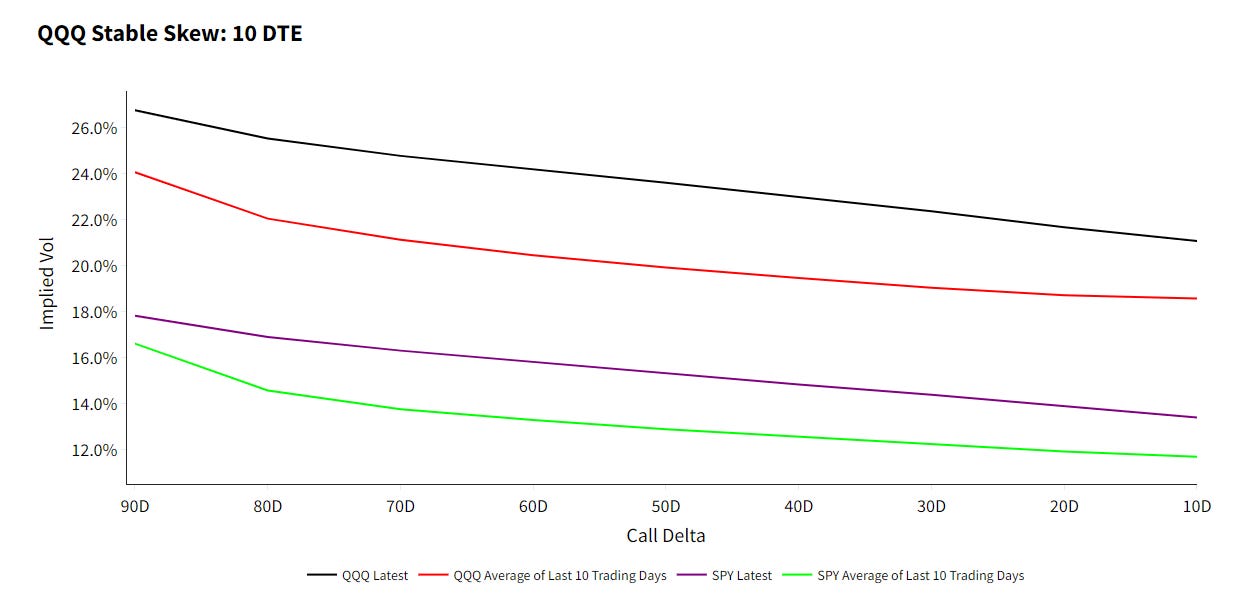

Between these known news events, and the recent price action, volatility is bid up across the board. SPY and QQQ ten day vols are up 2.5 and 3.5 points respectively for ATM options, compared to their ten day average.

With this macro environment as our backdrop, this week we look at issues through our filter of dividend yields. This can be both a leading and lagging indicator, as strong profits create the potential for high distributions, but falling stock prices also reduce the denominator.

When using the Screener to filter by dividend yield, the results are the most wide ranging of all of our indicators. It’s important to compliment this filter specifically with more fundamental research.

At Portfolio Design, we track opportunities through four different lenses: Volatility (VRP, IVNetHV), Liquidity (LIQ), Momentum/Mean Reversion (Bollinger) and Dividends. Each of these filters represents a different approach to investing, and can be used independently or in concert.

With these frameworks in place, follow along here twice a week as we dissect what the screens are telling us for Covered Call and Hedged Equity structures. Identify both short term trading and longer term investment opportunities. Free subscribers get a taste with “YIKES” and paid subscribers get analysis on the details of these opportunities, along with the full screener results.

Data comes from TheTape.Report where users can build their own screens and access a full suite of options indicators.

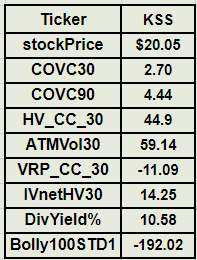

Yikes: KSS

Kohl’s has one of the most attractive dividend yields of our Top250, yet it’s also sitting amongst the furthest below its 100 day moving average. 10% yield sounds good, but not if your capital base is eroding away.

The other thing to pay attention here is the flip between IV, HV, and VRP. Earnings were released at the end of May, and are expected next on August 28th. We’re just starting to see a bit of that ATM vol getting bid up, and the gap between the 8/23 and 8/30 weeks that straddle the earnings is notable.

The biggest catch with a name like this however will be the width of markets. In the best cases they’re $0.30 wide, and that combined with $0.50 apart strikes means there might be some funny markets. For example this slight OTM call spread is $0.30 around even, with a midpoint of $0.04. That pricing tells you very little about “fair value”. For what it’s worth the smoothed vol value of that call spread is closer to $0.20.

Keep reading with a 7-day free trial

Subscribe to Portfolio Design with TheTape to keep reading this post and get 7 days of free access to the full post archives.